Pre-Purchase Price Allocation (Pre-PPA) – Why do it?

We understand that the merger and acquisition process is complex, and it is essential that the investor has as much information as possible to make an assertive and well-founded decision.

One of the strategic initiatives commonly adopted by investors to increase the chances of a transaction generating value is the Pre-Purchase Price Allocation, whose objective is the pre-measurement of the fair value of the business, the tangible and intangible assets acquired, and the respective preliminary measurement of Goodwill.

The Pre-PPA estimates the value of intangible assets not recorded on the balance sheet, which helps to predict the impact of the acquisition on the combined financial statements. Also, the Pre-Purchase Price Allocation allows the analysis of the tax benefits of both the amortization of intangible assets and the potential Goodwill. In Brazil, there is a scenario of a potential tax benefit of Goodwill, when it exists, as established by Law No. 12,973/14. According to this law, the Acquiring company may exclude, for purposes of calculating the Real Profit of the subsequent periods, the balance of Goodwill resulting from the acquisition between independent parties, in 60 months (if the company is incorporated).

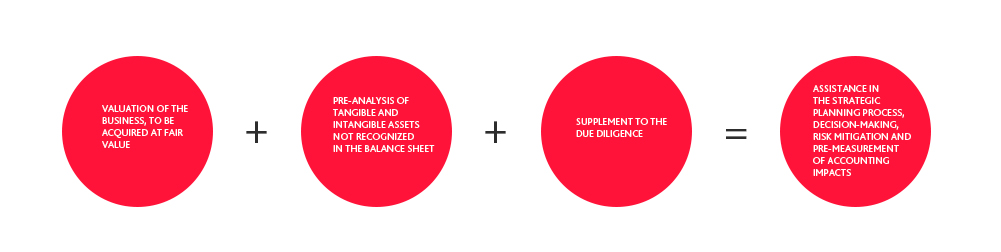

Therefore, the Pre-PPA offers the following benefits for strategic planning, decision-making, risk mitigation, and pre-measurement of accounting impacts:

- Valuation of the business at fair value: The Pre-PPA will measure in advance for the investor what would be the fair value of the business to be acquired (i.e. equity value, in a stand-alone manner and without specific synergies with the acquirer), which would be critical information for the investor for planning and decision-making purposes. In addition, the reconciliation between equity value and estimated purchase price is essential for compliance with the applicable accounting standard, IFRS 3 (CPC 15; US GAAP - ASC 805), of Business Combinations;

- Pre-valuation of assets: The Pre-PPA can bring valuable insights into the potential future transaction. The prior measurement of intangible assets, relating it to the potential drivers of business value, is essential for strategic and decision-making purposes. As an example, if it is understood that the customer relations is the main intangible asset to be acquired, the Pre-PPA will preliminarily estimate what the value of this asset would be, which is not recorded in the selling company's balance sheet. If any specific potential risk is identified in relation to customer relations, such as dependence on sales on a few customers or high churn-rate, the Pre-PPA will capture this in the evaluation. This information can, for example, be critical to define important issues, such as the price to be paid in the deal and the inclusion of earn-out clauses. In addition, as mentioned, the preliminary measurement of Goodwill itself can bring benefits in relation to tax planning; and

- Due diligence supplement: The Pre-PPA can complement the information obtained in the due diligence process, measuring the fair value estimate of the intangible assets acquired that are not recorded in the balance sheet at fair value, especially those that cannot be recognized internally, such as those related to the customer relations and brand.

Therefore, our team is prepared to help investors make well-supported and strategic decisions, and the Pre-PPA is an important tool that can help generate value in transactions.